With conditions remaining soft across most sectors of the UAE’s real estate market in 2018, the government launched a number of new initiatives to boost demand. In the year ahead, market performance will heavily depend on how quickly these investments and regulations have an impact, outlines JLL’s 2018 Year in Review report.

The general economic environment remained subdued in 2018 with UAE GDP growth at around 2%, a slight increase from 2017. In 2019 GDP is expected to grow at a slightly higher rate (3%) supported by an expansionary fiscal stance, continued investment ahead of Expo 2020 and higher government spending.

In 2018, the UAE government announced a number of relaxed regulatory controls to further drive economic diversification and stimulate weakened market demand. The introduction of a new 10-year residency visa and a 5-year retiree visa were launched to encourage investment and retain human capital in the Emirates, in turn reversing the current downturn in market conditions.

“Overall market sentiment should improve in the long run as the new visa regulations and economic stimuli will provide a boost to the UAE’s real estate market. However, the benefit of these initiatives is unlikely to have an immediate impact and 2019 is expected to remain a challenging year for most sectors of the real estate industry,” says Craig Plumb, head of research at JLL MENA.

Within the UAE, Dubai’s retail sector remains the most challenged because of ongoing increased supply. Retail also faces ongoing competition from e-commerce and although there have been efforts to drive the market with new entertainment concepts, future performance will rely on developers introducing new strategies to increase footfall and spend.

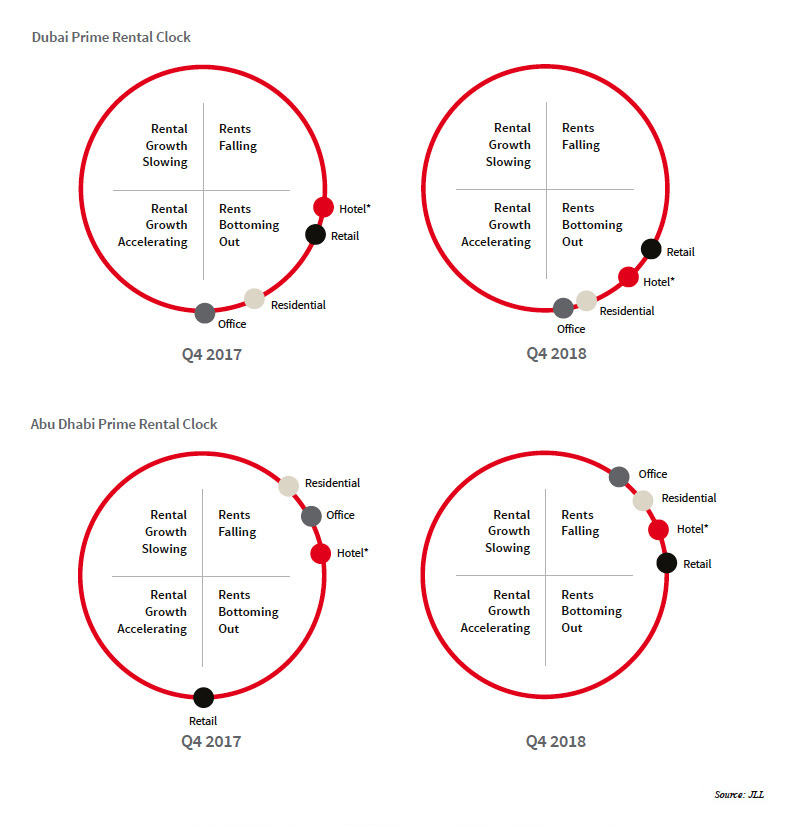

A look at Dubai’s retail real estate

Around 1.9 million sqft of retail GLA was completed in 2018, which is above the last five-year average of 1.7 million sqft. Q4 2018 saw the completion of The Pointe on Palm Jumeirah and the phase II of Marsa Al Seef on Dubai Creek, collectively adding 1.09 million sqft of retail GLA, bringing the total mall-based retail stock to around 39.8 million sqft at the end of 2018.

Looking ahead, notable projects expected to be delivered in the next two years include Nakheel Mall on the Palm Jumeirah, Dubai Hills Mall and Deira Islands.

There is around 14 million sqft of retail GLA expected to be delivered in the next two years with the supply expected to reach 55 million sqft by the end of 2020. This expected supply is dominated by super-regional malls (67%) with delays or the reduction in scale of these projects resulting in a significant reduction in the actual level of completions. The retail market currently faces the greatest danger of oversupply and more delays in future projects can therefore be anticipated.

Retail rents in primary and secondary malls declined by 13% and 22%, respectively, year-on-year. With the current market being tenant friendly, tenants are able to re-negotiate rents on favourable lease terms and landlords continue to offer concessions. Some landlords have also started sharing operating costs in addition to providing capital contributions to fit-outs. The large retail groups have been the biggest beneficiary of these concessions as they are able to negotiate special deals and turnover only rentals. Rents are expected to continue facing downward trend for the next 12 months.

The growing popularity of online retailing in the UAE is placing increased pressure on the performance of malls, with multiple online platforms having entered the market to capitalise upon this trend. According to Euromonitor, internet and mobile retailing constituted just 5% of the total retail sales in UAE in 2018, which is lower than the global average. This sector of the market is expected to grow rapidly over the next few years. While F&B has been a major growth sector in recent years, developers now need to introduce new strategies to increase footfall and sales with even the F&B sector reaching saturation level in some locations.

A look at Abu Dhabi’s retail real estate

There were no significant additions to stock recorded throughout the year, with the total retail stock remaining stable at approximately 29 million sqft GLA.

The retail market has witnessed the least deliveries of all sectors over the past three years with an average materialisation rate of just 23%. With market conditions remaining soft and developers remaining extremely cautious, only 17% of the retail space proposed for delivery in 2018 actually materialised.

Despite the declining market conditions, approximately 2.3 million sqft of retail GLA is currently scheduled to be delivered by the end of 2019. A large share of this supply is attributed to Al Maryah Central Mall, a super-regional mall coming up on Al Maryah Island. The remaining projects in the pipeline are mostly retail shops in mixed-use buildings as well as small neighbourhood and community malls. Beyond 2019, the most notable projects expected to be delivered include the proposed extension to Marina Mall and opening of Reem Mall.

Despite no significant new supply, tenants have had an increasingly strong negotiating position due to the increased level of vacant space as retailers have closed branches in Abu Dhabi.

While some tenants have been able to maintain an appropriate operating cost ratio, many have seen costs rise significantly as a percentage of sales. As a result, rent abatement periods and permanent reductions have been offered to tenants to maintain occupancy levels. Looking ahead, rents and occupancy levels in underperforming malls are expected to remain under pressure. Landlords are expected to offer more favourable leasing terms to retain existing tenants, in addition to adopting innovative leasing and marketing strategies to maximise engagement with shoppers.

Lulu Retail, the GCC’s retail powerhouse, has reported a transformative FY 2024,

The Ministry of Industry and Advanced Technology (MoIAT) in cooperation with Lulu

What does it take to sustain profitable growth in the post-IPO phase?

Mahalle began its operations in 2022 as an “Authentic Turkish Grocery in

NRF Vice President of Education Strategy Susan Reda forecasts 2025’s retail trends

The Dubai Duty Free (DDF) has recorded sales of $1.94 billion up

Saudi Arabia’s retail sector is rapidly transforming under Vision 2030. E-commerce, brick-and-mortar

At the heart of retail lies the consumer, Deloitte pointed out while

Notifications