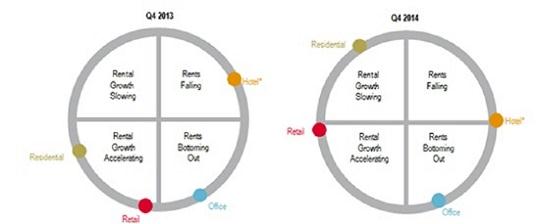

Jones Lang LaSalle (JLL) has released its fourth quarter (Q4 2014) Riyadh Real Estate Overview report that asses the latest trends in the retail, hotel, office and residential sectors in Saudi Arabia’s largest city.

Commenting on the Riyadh market report, Jamil Ghaznawi, national director and country head of JLL KSA, observes, “Confidence in the retail market remains strong as reflected in the announcement of various new shopping centres, positively effecting rental growth figures. Supply increases in the hotel sector that showed occupancy rates were improving and average daily rates remain under downward pressure. While in the office sector, new supply has constrained performance and increased vacancies. In the last quarter of 2014, we have also witnessed the introduction of new mortgage regulations requiring a 30% down payment on all home financing; this has restricted growth levels in the residential market.”

The retail segment saw no new completions over the last quarter, as only smaller retail centres were delivered – for example Meem Plaza. Rents have slightly increased in regional and community shopping centres, whereas super regional malls saw no increase. Vacancy levels in major malls have slightly decreased (-1%) during this quarter. Delays in the KAFD and ITCC projects have resulted in their retail components being pushed back into 2015 and beyond.

“The Saudi real estate market is heavily dependent upon high levels of government spending and while the more prudent approach is unlikely to have an immediate impact on the market in 2015, it certainly marks the end of a period of rapid increase in spending, which could constrain the growth of the real estate market in the longer term,” adds Ghaznawi.

Watsons to open 20 new stores in the GCC

In 2020, global health & beauty retailer AS Watson Group signed its

April 29, 2024 | By Rupkatha B

The Ministry of Industry and Advanced Technology (MoIAT) in cooperation with Lulu

What does it take to sustain profitable growth in the post-IPO phase?

Mahalle began its operations in 2022 as an “Authentic Turkish Grocery in

“Retail is a people’s business. When building a retail brand or the

From being one of the first retailers in Dubai to ban single-use

For starters, Rabbit is a growing e-commerce grocery platform in Egypt always

In 2024 grocery retail major Choithrams has achieved several milestones underscoring its

Industry pioneers are embracing a comprehensive strategy that integrates consumer insights, digital

The regional grocery retail market is evolving fast keeping pace with constantly

From ethical and local sourcing to adopting cutting-edge technologies to curb food

Finding the treasure chest of opportunities needs years of journeying through the

How is the food service industry in the Kingdom of Saudi Arabia

The fusion of global and local trends will support the fashion industry

Numerous homegrown brands from the Kingdom of Saudi Arabia are spreading wings

How is the retail industry adapting to rapidly changing consumer behaviour –

While it may not reach the heights of 20-25% penetration, the e-commerce

With coffee being a preferred beverage, the GCC coffee industry has seen

Forty-four percent of TikTok users in the GCC buy something to fit

A frictionless omnichannel experience which is predictive, value-focused, and highly personalised is