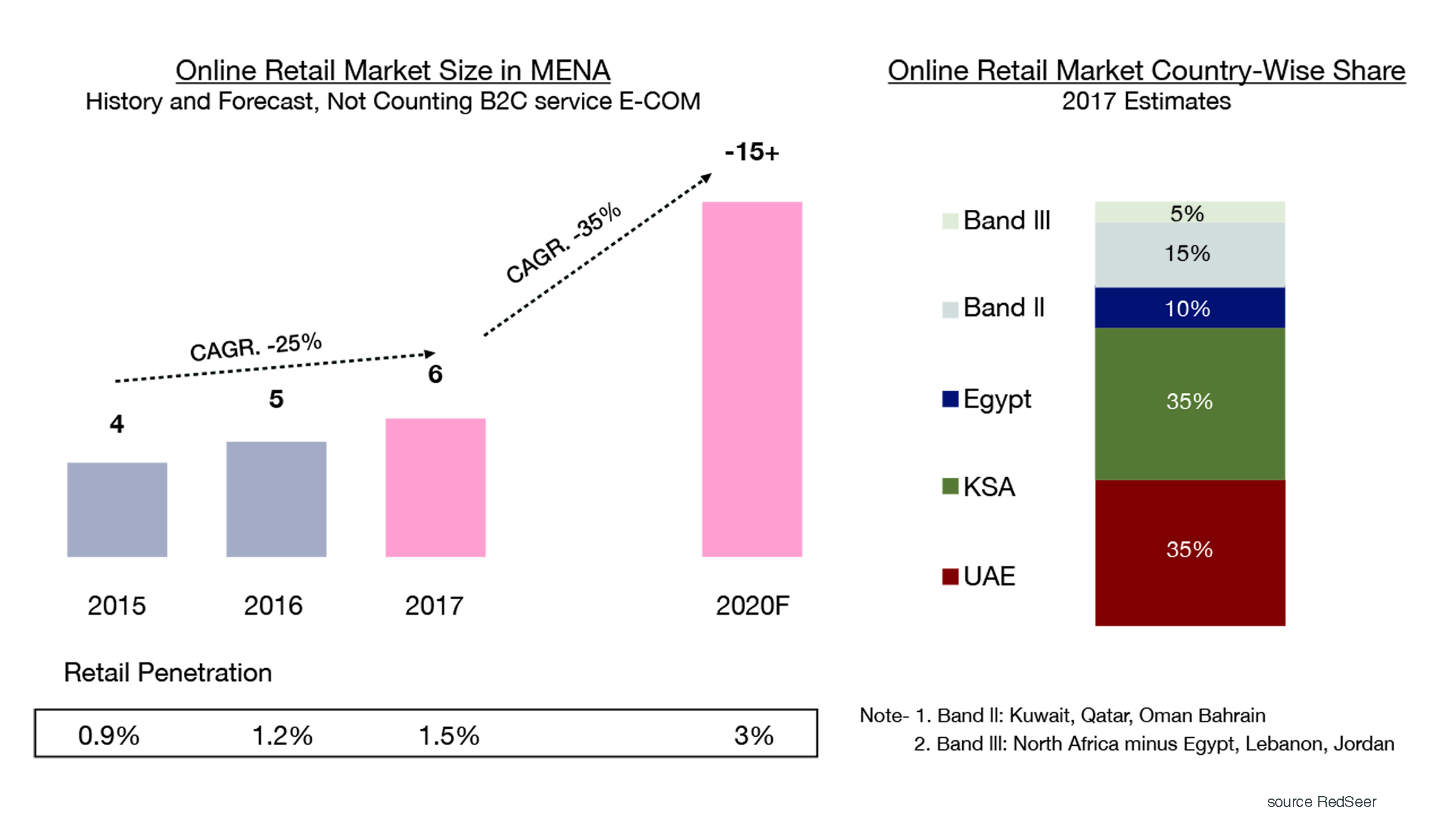

The Middle East e-commerce market is heating up with increasing competition, driven primarily by the UAE and Saudi Arabia. According to estimates, from 2015-17, the MENA online retail market went from $4 to $6 billion. By 2020, the MENA e-commerce market is estimated to surpass $15 billion at 35% CAGR. The UAE and Saudi Arabia will remain the largest and fastest-growing e-commerce markets in the region, with consumer electronics and fashion being the strongest categories.

In the background of these developments, the UAE arm of RedSeer, the consumer internet focused research and advisory firm in emerging markets, has come out with an e-commerce study of the MENA region.

MENA’s online retailers have had to contend with myriad challenges – be it poor transport and payment infrastructure, low customer awareness and trust or limited selection – which contributed to stunting the online growth. However, funding from significant investors recently is leading to a wave of infrastructure development and substantial investment on building a strong value proposition for the customer – all of which will drive rapid growth in online across the region.

SOUQ continues to be the market leader with 15%+ market share. It is continuously increasing its presence in GCC and North Africa.

Jumia with its large customer base coming from African countries is the second biggest player with 8%+ market share.

noon has picked up fast in last one year to gain 3%+ market share. It launched festive offers like ‘Yellow Friday’ in 2018 to compete with ‘White Friday’ offers from SOUQ.

Namshi is the leading fashion player in the region. The company has been recently acquired by Emaar Malls, which has a stronghold in offline retail. The two together are expected to drive omnichannel retail in the coming years.

From being a marketplace, Wadi’s focus has now shifted to online grocery in KSA, after Majid Al Futtaim – with its Carrefour operations – bought a strategic stake by investing $30 million in Wadi.

International cross border trade (CBT) continues to contribute significantly to the MENA e-tailing market. However, its share has dropped 30% from 35% in 2016.

Read the full article, to be exclusively published in the January edition of RetailME

Watsons to open 20 new stores in the GCC

In 2020, global health & beauty retailer AS Watson Group signed its

April 29, 2024 | By Rupkatha B

The Ministry of Industry and Advanced Technology (MoIAT) in cooperation with Lulu

What does it take to sustain profitable growth in the post-IPO phase?

Mahalle began its operations in 2022 as an “Authentic Turkish Grocery in

“Retail is a people’s business. When building a retail brand or the

From being one of the first retailers in Dubai to ban single-use

For starters, Rabbit is a growing e-commerce grocery platform in Egypt always

In 2024 grocery retail major Choithrams has achieved several milestones underscoring its

Industry pioneers are embracing a comprehensive strategy that integrates consumer insights, digital

The regional grocery retail market is evolving fast keeping pace with constantly

From ethical and local sourcing to adopting cutting-edge technologies to curb food

The Dubai Duty Free (DDF) has recorded sales of $1.94 billion up

Saudi Arabia’s retail sector is rapidly transforming under Vision 2030. E-commerce, brick-and-mortar

At the heart of retail lies the consumer, Deloitte pointed out while

The GCC retail industry is projected to grow at a compound annual

In what comes as a significant announcement, Middle East based eyewear majors

Emirati Gen Z women are seeking collaborative, culturally diverse and creatively enriching

The retail landscape in the Middle East is undergoing a seismic shift,

GMG’s Everyday Goods – Retail division celebrates expansion milestone hitting 60 stores

Among several others, three key factors have fuelled the growth of homegrown